When evaluating land, one concept stands above the rest in determining value, opportunity, and long-term potential: highest and best use analysis.

At its core, this analysis answers a critical question: What is the most profitable and productive use of this land—now or in the future?

For buyers, this means identifying hidden upside. For sellers, it means positioning a property to capture its full market value. Whether you’re looking at farmland, ranchland, or property on the edge of a growing town, understanding highest and best use can completely change how you view a piece of land—especially when browsing farm land for sale in competitive markets.

What Is Highest and Best Use in Real Estate?

Highest and best use refers to: The most reasonably probable use of a property that results in the highest value.

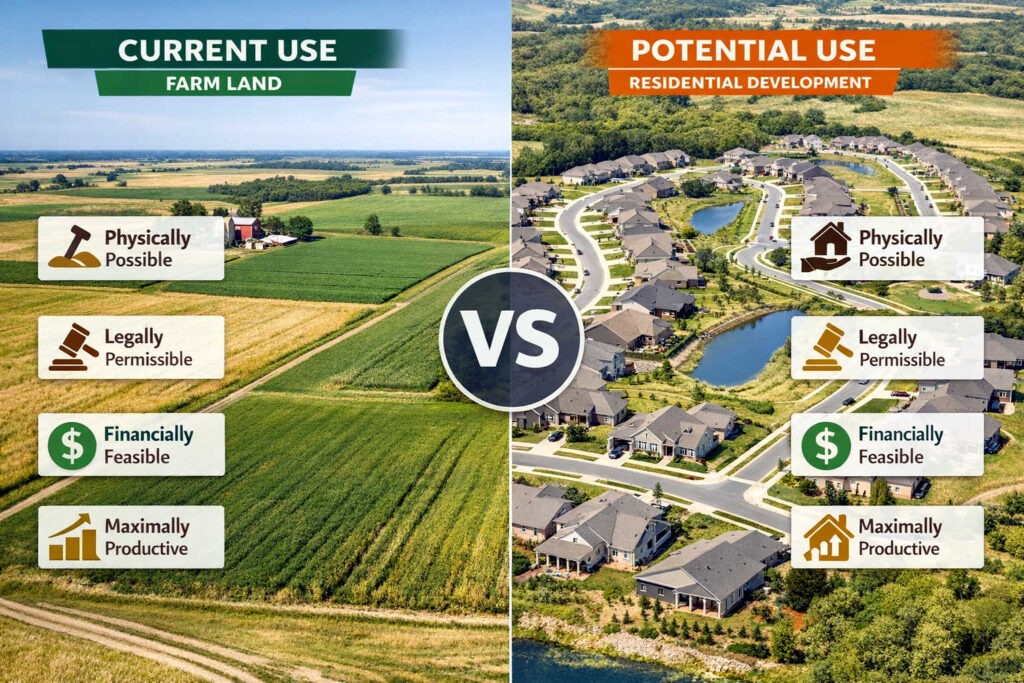

It’s important to understand that highest and best use is not always the current use.

A property might:

- Be used as pasture today

- But have significantly greater value as residential development

Or:

- Operate as dryland farming

- But become far more valuable with irrigation improvements

The difference between what land is and what it could be is where opportunity—and profit—lives.

What Is a Highest and Best Use Analysis?

A highest and best use analysis is commonly used by professionals in the appraisal industry, including organizations like the Appraisal Institute, to determine the most valuable use of a property.

Rather than guessing, this analysis evaluates the land through a combination of:

- Physical characteristics

- Legal constraints

- Financial feasibility

- Market demand

The goal is simple. Identify the use that produces the maximum value while remaining realistic and achievable

This process is used by:

- Land brokers

- Appraisers

- Investors

- Developers

And it plays a major role in both buying decisions and pricing strategy.

The 4 Tests Used in a Highest and Best Use Analysis

To qualify as the highest and best use, a potential land use must pass four key tests.

1. Physically Possible

What can the land realistically support? Resources like the USDA Natural Resources Conservation Service provide valuable soil and land data that can help determine what a property can realistically support.

This includes:

- Soil quality

- Topography

- Access (roads, utilities, water)

- Climate and drainage

For Example: Flat, fertile ground with access to water may support row crop production, while rough or heavily wooded terrain may be better suited for grazing or recreation.

2. Legally Permissible

What is allowed under current regulations? Environmental regulations enforced by agencies such as the U.S. Environmental Protection Agency can also impact how land may be used or developed.

This includes:

- Zoning laws

- Deed restrictions

- Environmental regulations

For Example: Even if land is ideal for commercial development, zoning may restrict it to agricultural use unless rezoning is approved.

3. Financially Feasible

Will the use generate a return?

This involves:

- Acquisition cost

- Development expenses

- Market demand

- Comparable sales

For Example: Subdividing land into residential lots may be physically possible—but not financially feasible without strong local demand.

4. Maximally Productive

Which use creates the highest value?

This is the final step, where all factors come together.

For Example: If land can be used for:

- Grazing ($2,000/acre value)

- Irrigated farming ($6,000/acre value)

Then irrigated farming would be considered the highest and best use.

Real-World Examples of Highest and Best Use in Land

Understanding theory is one thing—seeing it applied is where it becomes powerful.

Agricultural Land

- Current Use: Dryland farming

- Potential Use: Irrigated farming

- Key Driver: Water access and soil quality

Adding irrigation can significantly increase yield—and land value, especially when evaluating Nebraska farm land for sale or similar agricultural markets.

Transitional Land (Path of Growth)

- Current Use: Pasture or farmland

- Potential Use: Residential or commercial development

- Key Driver: Nearby city expansion

This type of land often sees the biggest jumps in value over time.

Recreational Land

- Current Use: Hunting property

- Potential Use: Cabin sites or short-term rentals

- Key Driver: Location, access, and natural features

Value can increase when land supports multiple income streams.

Why Highest and Best Use Analysis Matters

A highest and best use analysis isn’t just theoretical—it directly impacts real-world decisions. Buyers evaluating Kansas farm land for sale can use highest and best use analysis to identify undervalued opportunities and long-term investment potential.

Determines Property Value

Land is valued based on its potential, not just its current use.

Guides Investment Decisions

Buyers can identify:

- Undervalued properties

- Future development opportunities

- Land with hidden upside

Improves Pricing Strategy

Sellers who understand highest and best use can:

- Price more accurately

- Market more effectively

- Attract the right buyers

Strengthens Land Marketing

Listings that clearly communicate potential uses:

- Generate more interest

- Appeal to investors and developers

- Stand out in competitive markets

How to Perform a Highest and Best Use Analysis

While professional appraisals provide the most reliable results, buyers and sellers can begin evaluating land by following a structured approach.

Step 1: Evaluate Physical Characteristics

- Review soil maps, topography, and access

- Conduct a land survey if needed

Step 2: Verify Legal Constraints

- Check zoning regulations

- Review deed restrictions and easements

- Understand environmental limitations

Step 3: Analyze Financial Feasibility

- Estimate development costs

- Compare with market values

- Review comparable land sales

Step 4: Compare Potential Uses

- Identify multiple possible uses

- Determine which produces the highest return

Can You Do a Highest and Best Use Analysis Yourself?

Yes—but it requires time, research, and local knowledge.

Successful land buyers and sellers often rely on:

- Experienced land brokers

- Appraisers

- Local planning authorities

This ensures decisions are based on accurate data rather than assumptions

Frequently Asked Questions About Highest and Best Use Analysis

What is highest and best use analysis in real estate?

Highest and best use analysis is the process of determining the most profitable and productive use of a piece of land. It evaluates physical characteristics, legal restrictions, financial feasibility, and market demand to identify the use that results in the highest value.

What are the four tests of highest and best use?

The four tests of highest and best use are: physically possible, legally permissible, financially feasible, and maximally productive. A property must meet all four criteria for a use to be considered its highest and best use.

Is highest and best use always the current use of the land?

No, highest and best use is not always the current use. Land may be used one way today but have greater value if used differently in the future, such as farmland transitioning to residential development.

Who performs a highest and best use analysis?

Highest and best use analysis is typically performed by licensed appraisers, land brokers, and real estate professionals. Investors and buyers may also conduct their own analysis when evaluating land opportunities.

Why is highest and best use important when buying land?

Understanding highest and best use helps buyers identify the true potential of a property. It can reveal opportunities for increased value, better investment returns, and more strategic land use decisions.

How does highest and best use affect land value?

Land value is largely determined by its highest and best use. Properties that support more profitable or in-demand uses typically have higher market values than those with limited or less productive uses.

Can zoning changes affect highest and best use?

Yes, zoning changes can significantly impact highest and best use. If land is rezoned to allow for more intensive or valuable uses, its potential value and development opportunities may increase.

Can you perform a highest and best use analysis yourself?

Yes, but it requires research and local knowledge. Evaluating zoning, market trends, physical characteristics, and financial feasibility can be complex, so many buyers and sellers choose to work with experienced professionals.

What is the difference between highest and best use and market value?

Highest and best use determines the most valuable potential use of a property, while market value is the price a buyer is willing to pay. The two are closely related, as market value is often based on the property’s highest and best use.

Final Thoughts: Look Beyond What the Land Is Today

One of the biggest mistakes in land real estate is evaluating property based only on its current use. If you’re currently exploring farm land for sale, applying a highest and best use analysis can help you identify properties with the greatest upside and long-term value.

The real opportunity lies in asking: What could this land become?

A well-executed highest and best use analysis allows you to:

- Make smarter investments

- Maximize property value

- Identify opportunities others overlook

Whether you’re buying, selling, or simply evaluating land, understanding highest and best use gives you a clear advantage in the market.